AI Companion Investment Data: Funding & VC Deals 2026

The AI companion app space has quietly become one of the most aggressively funded corners of consumer tech — and most people are still sleeping on just how much money has moved into it.

This is not a market-size article. The revenue breakdown, platform earnings, and ARPU data live in our AI Companion Industry Revenue piece. This one is strictly about the investment side: who is writing the cheques, how much they are putting in, what valuations look like, and where the M&A activity is heading.

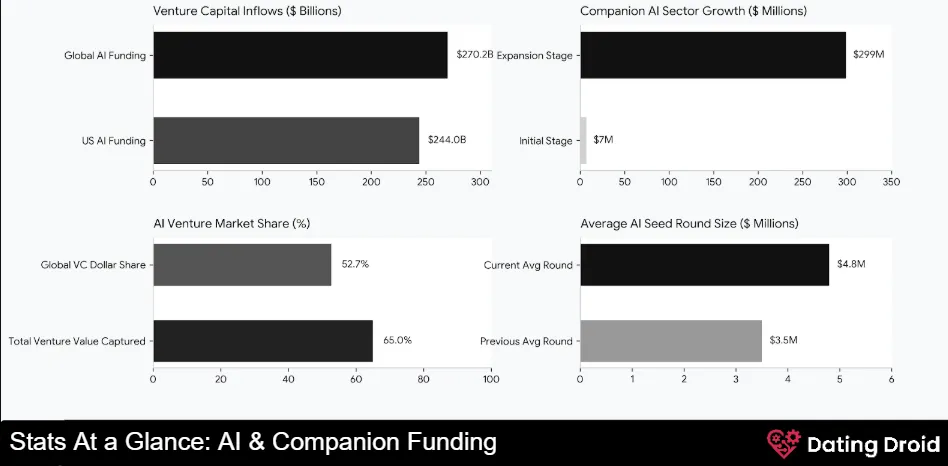

⚡ AI Companion Investment in 2026: Key Funding Stats at a Glance

Before getting into individual deals, here is the macro-level capital environment that AI companion startups are raising into:

Capital is concentrating into fewer, larger bets — and AI companion and emotional AI startups are sitting right in the crosshairs.

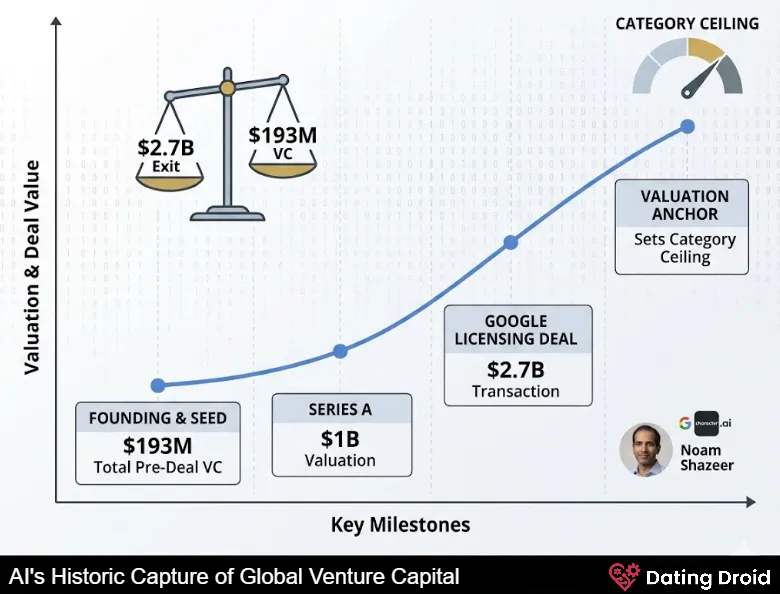

💰 Google's $2.7B Character.AI Deal: The Biggest AI Companion Acquisition Ever

No transaction has shaped AI companion app valuations more than the Google × Character.AI deal closed in August 2024.

Google paid $2.7 billion in a non-exclusive LLM licensing agreement that doubled as an acqui-hire — bringing Character.AI founder Noam Shazeer and core team back under Google's roof. The U.S. Department of Justice opened an antitrust investigation into the deal structure shortly after.

Character.AI Funding Timeline & Valuation History

| Round | Date | Details |

|---|---|---|

| Series A | March 2023 | $150M led by Andreessen Horowitz; $1B valuation |

| Rumoured mega-round | Sept 2023 | $5B+ valuation floated — never closed |

| Google LLM licensing deal | August 2024 | $2.7B total; investor buyout at ~$2.5B valuation |

| DOJ investigation | Late 2024 | Antitrust scrutiny on deal structure |

Character.AI's total disclosed VC pre-deal: a comparatively modest $193 million. The $2.7B exit is the largest payout in AI companion history — and it permanently anchored the valuation ceiling for every other platform in the category.

🔥 Replika Funding History & Valuation

Here is the plot twist every AI companion investor should be staring at: Replika — the platform that invented the category — built a profitable business on essentially zero outside money.

After a $6.5M Series A from Khosla Ventures in 2017, Replika raised nothing. No follow-on rounds. The company scaled to 10 million downloads, did $14M ARR in 2024 (verified via GetLatka), and currently sits at an estimated $41.9M valuation.

In a category where most startups are torching VC cash chasing growth, Replika has been profitable and founder-controlled for years. Eugenia Kuyda answers to nobody — and that is its own kind of flex.

📲 Major AI Companion App Funding Rounds (2024–2026)

Beyond Character.AI and Replika, here are the most significant AI companion investment deals worth tracking.

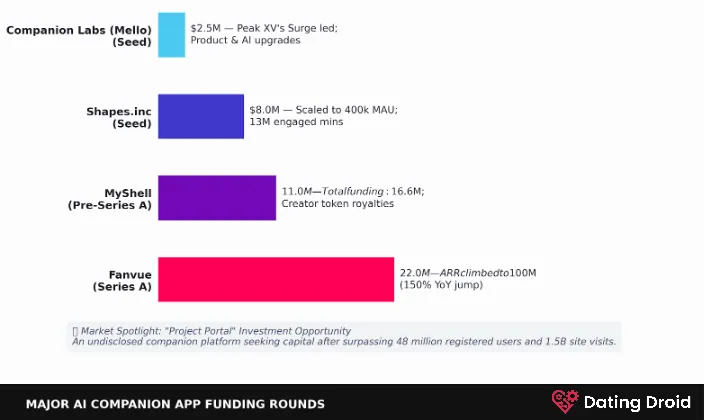

MyShell Funding ($11M Pre-Series A)

Tokyo-based MyShell — a decentralised platform for building AI girlfriends and productivity bots — closed an $11M Pre-Series A in March 2024 led by Dragonfly Capital, bringing total funding to $16.6M. Backers included Delphi Ventures, OKX Ventures, Nomad Capital, Maven11 Capital, and Nascent. Angel investors included ex-Coinbase CTO Balaji Srinivasan and NEAR Protocol co-founder Illia Polosukhin.

The blockchain-meets-AI-girlfriend thesis is genuinely novel: creators who build characters on MyShell earn token-based royalties from their personas. Think OnlyFans economics — but the creator is an AI persona and the payout is in crypto.

Shapes.inc Funding ($8M Seed)

Shapes came out of stealth in April 2026 with an $8M seed round led by Lightspeed Venture Partners, with AI Capital Partners and AI Grant joining. The Georgia Tech-founded startup had already scaled to 400,000 monthly active users by end of Q1 2026 — a six-fold increase since January 2026. Users collectively logged 13 million engaged minutes in March 2026 alone.

Their bet: instead of deeper one-on-one AI attachment, treat AI as a social layer between real friends. A direct counter-position against the social isolation narrative attached to solo AI companion use.

Companion Labs Mello Funding ($2.5M Seed)

India's first institutional AI companion bet. Pune-based Companion Labs, building the AI companion app Mello, closed a $2.5M seed round in February 2026 led by Peak XV's Surge (formerly Sequoia India), with All in Capital, DeVC, and UntitledVC joining. Capital is earmarked for product development and AI model upgrades.

India has one of the fastest-growing user bases for AI chat apps globally. This is likely the first of many institutional bets on Indian-built companion platforms.

Fanvue Funding ($22M Series A)

Adult creator infrastructure platform Fanvue closed a $22M Series A in 2026 as ARR climbed to $100M — a 150% year-over-year jump from $40M in 2024. While Fanvue is technically platform infrastructure rather than a companion app, its embrace of fully synthetic AI creator personas makes it core to the AI companion investment landscape. Fansly banned photorealistic AI content; Fanvue went the other direction and leaned in fully.

Project Portal Investment Opportunity

ACF Investment Bank presented an AI companionship platform investment opportunity in May 2026 for a platform that has surpassed 1.5 billion site visits in under 2.5 years with 48 million registered users — one of the largest undisclosed companion platforms currently being positioned for outside capital.

🆚 AI Companion App Valuations vs. Funding Raised

The gap between disclosed funding and actual valuation in this category is worth paying attention to.

| Platform | Total Funding Raised | Estimated Valuation | Notes |

|---|---|---|---|

| Character.AI | $193M disclosed | $2.7B (Google deal, 2024) | Acqui-hire structure |

| Replika | $6.5M (2017 only) | ~$41.9M | Fully bootstrapped post-2017 |

| MyShell | $16.6M | Undisclosed | Blockchain + AI GF model |

| Fanvue | $22M Series A | Implied ~$200M+ | $100M ARR platform |

| Shapes.inc | $8M seed | Early stage | 400K MAU at seed |

| Companion Labs | $2.5M seed | Early stage | First Indian institutional bet |

The Character.AI deal made one thing explicit: the proprietary LLM and the emotional engagement model are the asset, not just the user count. Google did not pay $2.7B for 20 million MAU — it paid for the model and the team that built it.

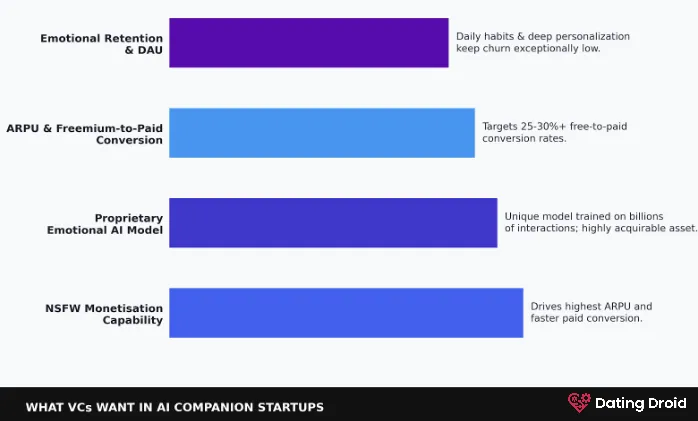

✨ What VCs Want in AI Companion Startups

Investment criteria for AI companion and AI girlfriend app startups have shifted significantly since 2022. Early-stage backers chased download numbers. Now the metrics that matter are:

Emotional Retention & DAU

How many users come back daily, and for how long. AI companion apps with memory, voice, and personalisation retain users at rates most social apps cannot match. An emotionally attached user is a paying user who does not churn.

ARPU & Freemium-to-Paid Conversion

Revenue per download jumped from $0.52 to $1.18 in a single year (2024–2025). Platforms converting free users to paid subs at 25–30%+ are the targets.

Proprietary Emotional AI Model

The Character.AI deal proved it: if your platform has trained a unique emotional AI model on billions of companion interactions, that model is a separable, licensable, acquirable asset.

NSFW Monetisation Capability

The one most institutional VCs won't say out loud — but the data is obvious. NSFW AI companion platforms generate significantly higher ARPU than SFW equivalents and convert to paid tiers faster.

Web-First vs. App Store Model

Pure mobile apps face the 30% app store revenue cut. Platforms with web-first or hybrid architectures sidestep both the revenue tax and the content restriction risk.

👀 AI Companion App M&A Outlook: Who Gets Acquired Next

The Character.AI deal opened the template. Here is how AI companion acquisitions are likely to unfold from here.

Big Tech Acqui-Hires of AI Companion Startups

The most probable exit for founder-led AI companion startups with strong underlying models. Any platform that has built a genuine proprietary emotional AI stack — not just wrapped an existing LLM — is a target for Google, Meta, Microsoft, or Amazon. License the model, hire the founders, absorb the IP.

NSFW AI Platform Consolidation & Roll-Ups

The less-discussed but structurally inevitable trend. With 300+ NSFW AI apps competing for the same user pool, economics favour roll-up acquisitions. A well-funded platform acquiring 10–15 NSFW AI players could rapidly consolidate the most monetisable segment of the market.

Health Tech Crossover Acquisitions of Emotional AI Apps

The sleeper bet. Replika has spent years positioning itself as a mental wellness tool. Any health tech company looking to add an AI-native engagement layer with proven daily retention data has a clear acquisition thesis here.

AI Voice & Infrastructure Tooling M&A

Platforms like ElevenLabs ($330M ARR) already power the voice layer of multiple AI companion apps. As the companion app market matures, infrastructure companies (voice, image generation, memory APIs) become the most defensible acquisition targets of all.

💸 AI Companion Seed-Stage Funding Gap: The Underfunded Opportunity

Around 3,200 seed-stage AI deals closed globally in 2025 with an average round size of $4.8M. Series A rounds for AI-native startups now achieve median valuations exceeding $50M.

The AI companion segment specifically remains underfunded relative to revenue performance. A category generating $120M+ in mobile consumer revenue, growing 64% year-over-year, with ARPU doubling in 12 months — and the majority of platforms are still bootstrapped or have raised under $20M.

That gap between commercial performance and institutional investment is not going to last. The Companion Labs deal in India, the Shapes.inc raise from Lightspeed, and the Project Portal investment opportunity all signal that institutional capital is finally taking the category seriously at the seed and Series A level — not just at the Character.AI mega-deal level.

The next 24 months will almost certainly produce the first dedicated AI companion–focused VC fund. That is not speculation — it is pattern recognition.

Stay Updated with Us

📌 AI Companion Investment FAQ

Who has invested the most in AI companion apps?

Google has the largest single position via its $2.7B Character.AI deal (2024). Andreessen Horowitz led Character.AI's $150M Series A. Lightspeed (Shapes.inc), Peak XV's Surge (Companion Labs), and Dragonfly Capital (MyShell) are the most active AI companion VCs in 2025–2026.

What is the largest AI companion acquisition?

The Google × Character.AI deal at $2.7 billion in August 2024 — by far the largest AI companion-related transaction recorded.

How much funding has Replika raised?

Replika raised $6.5M in a 2017 Series A from Khosla Ventures, and has been fully bootstrapped since. Current estimated valuation: $41.9M.

Are NSFW AI companion apps getting institutional VC funding?

Mostly indirectly. Adult-friendly infrastructure plays like Fanvue ($22M Series A) and Web3 platforms like MyShell ($16.6M total) are funded. Most pure NSFW companion apps remain bootstrapped or rely on revenue-based financing.

What is the average AI startup seed round size in 2025?

$4.8M, up from $3.5M in 2024. AI seed rounds now command roughly 35% larger cheques than non-AI equivalents.