AI Companion Industry Revenue: Who’s Making the Most?

The AI companion industry is sitting on a very real pile of cash — and most of it is flowing to a small, ruthless group of winners. In 2025, mobile AI companion apps alone crossed $120 million in annual consumer revenue. The broader AI companion market hit $37.12 billion when you count all platform types, and it is not slowing down.

But here is the part nobody puts in the press release: the money is not shared equally. Not remotely.

This article breaks down where every dollar in the AI companion industry revenue chain actually goes — which platforms dominate the earnings table, how the monetisation models work behind the scenes, who is quietly winning the NSFW lane, and what the solo creator economy actually looks like when you get past the LinkedIn case studies.

(Already covered the market size forecasts and user behaviour breakdowns in our AI Girlfriend Statistics and AI Dating App Download Statistics articles. This one is purely about the money.)

✨AI Companion Industry Revenue at a Glance

Mobile AI companion apps generated $82 million in H1 2025 alone — a 64% jump year-over-year. By end of 2025, the category hit its $120M+ annual revenue run rate, confirmed by Appfigures' data.

The broader AI companion market, inclusive of web platforms and adult subscription infrastructure, is valued at $37.12 billion globally in 2025, per Precedence Research.

Here is what makes those numbers interesting:

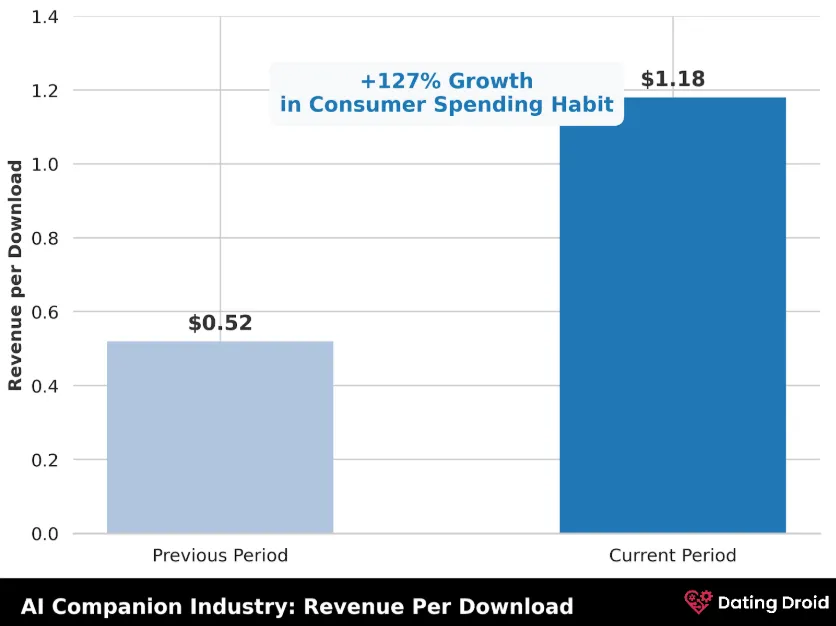

Users are not just downloading these apps for a look anymore. They are paying for them — month after month — and the revenue per download doubling in one year signals a market that has moved firmly from curiosity to habit.

🔥 Top-Earning AI Companion Platforms, Ranked

The AI companion space runs on winner-takes-most logic, and the data backs this up hard. The top 10% of apps capture 89% of total category revenue. Everyone else is competing for the table scraps left by the top 33 performers.

Here is the most up-to-date revenue picture across the main platforms, based on verified 2025–2026 data:

| Platform | Active Users | Verified Revenue (2025) | Notes |

|---|---|---|---|

| Chai AI | 1M+ DAU | $58M–$85M ARR | Closed 2025 at $58M ARR; hit $85M/yr run rate by April 2026 |

| Fanvue | 17M MAU, 250K creators | $100M ARR | Up 150% YoY from $40M in 2024; $22M Series A in 2026 |

| Candy AI | 1.5M MAU | $25M ARR | Fully bootstrapped; ~$5.6M estimated monthly revenue |

| Replika | 10M+ downloads | ~$14–35M ARR | $14M confirmed 2024 (GetLatka); $35.1M Growjo estimate |

| Character.AI | 20M MAU | ~$32.2M ARR | From subscription revenue; Google licensing deal valued separately |

A few things worth calling out here.

Chai AI is the story nobody saw coming. The platform opened 2025 at $20M ARR, hit $48M by October 2025 — two months ahead of its own internal target — closed the year at $58M ARR, and then reached an $85M annualised run rate by April 2026. That is a 3x growth in under 15 months, backed by a $30M investment from AMD and a 2.7x year-over-year user growth rate.

Fanvue is in a class of its own when you include adult AI creator monetisation. Sacra confirmed the $100M ARR figure in January 2026, up from $40M in 2024. AI-generated personas now account for approximately 15% of Fanvue's total ARR — roughly $15M coming entirely from synthetic creators. Top AI performers on the platform are clearing $20,000+ per month.

Character.AI generates ~$32.2M in subscription revenue. That figure looks modest next to its $1 billion valuation and the noise around its 40M+ download count — but downloads and revenue are two very different games.

Candy AI, completely bootstrapped with zero VC funding, sits at $25M ARR with a reported ARPU of $7.50/month and 30% of its user base as paying subscribers. Clean numbers for a clean operation.

Replika's figures vary significantly across sources — $14M is the verified 2024 figure from GetLatka; Growjo's model puts estimated annual revenue at $35.1M. The truth likely sits somewhere in between for 2025.

⚡ How AI Companion Apps Actually Monetise

There is no single dominant model here. The platforms making real money stack multiple revenue layers, and understanding how they do it explains why some apps print cash while hundreds of competitors go quietly dark.

Subscription Tiers

Subscriptions are the foundation. The model held a 25.38% revenue share in 2024 and continues to dominate across both mainstream and NSFW companion platforms.

Typical pricing structure across the market in 2026:

Monthly recurring revenue is predictable and sticky. The longer a user has emotionally invested in one AI companion — built a name, a backstory, a dynamic — the lower the churn. That emotional attachment loop is what makes the subscription model so durable in this category.

Freemium-to-Premium Funnels

Freemium is the fastest-growing monetisation approach at 24.07% CAGR. On Candy AI specifically, 70% of users are on the free tier — feeding a conversion funnel to the 30% who pay.

The mechanics are straightforward: give users a functional, emotionally engaging free experience, then put the things they genuinely want behind a paywall.

What sits behind the lock:

The free tier is not generosity. It is a highly optimised conversion engine.

PPV, Tipping & Sexting Bundles

A growing number of platforms have lifted the monetisation playbook straight from OnlyFans — and it works. Pay-per-view content drops, tipping on chat sessions, and bundled sexting or “custom scenario” packages are now standard across NSFW-facing companion apps.

This layer stacks on top of subscriptions rather than replacing them. A user paying $24.99/month will still tip for a custom scenario or spend separately on an exclusive image drop. Fanvue's infrastructure enables this exact model — subscriptions, PPV, tips, and voice messages all running simultaneously per creator. Platforms like Lovescape AI have built referral-and-earn mechanics on top of this structure, effectively turning their user base into unpaid acquisition agents.

The result: ARPU on NSFW companion platforms runs significantly higher than on mainstream equivalents. The engagement loop is tighter, and users with higher emotional or sexual investment spend more per session.

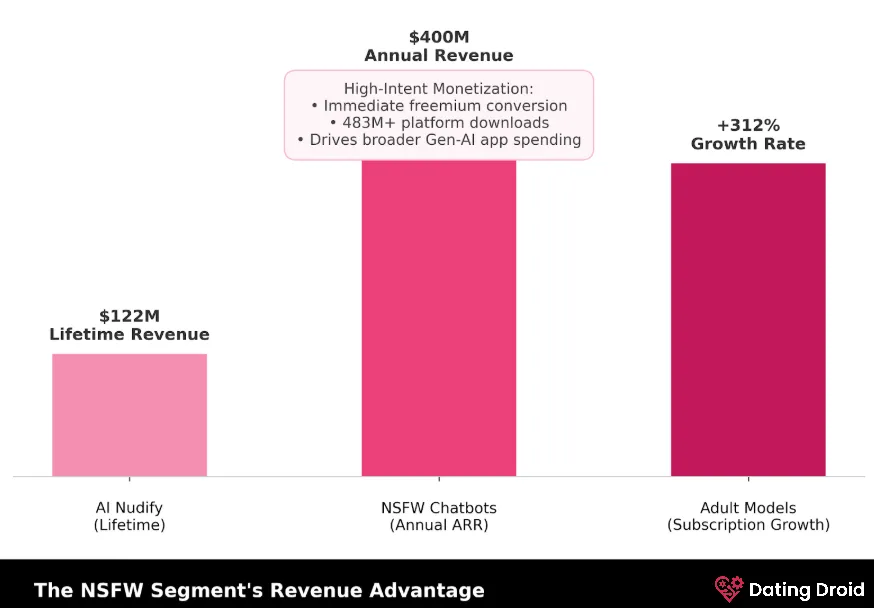

📈 The NSFW Segment's Revenue Advantage

This is where the real bag is stuffed.

NSFW AI is not just a lane inside the AI companion market — by early 2026, it is the single most commercially potent segment within it. The figures speak plainly:

NSFW platforms monetise faster than mainstream companions for a structural reason: user intent. Someone who opens a mainstream companion app might want emotional support, casual chat, or social skill-building. Someone who opens an adult AI platform knows exactly what they want — and they will pay for it with minimal friction.

Freemium conversion is also tighter in adult AI. The locked content is more immediately compelling, so the time from “free user” to “paying subscriber” is shorter. You are not waiting weeks for emotional attachment to develop. Conversion often happens within the first or second session.

The AI nudify and AI porn generation segment represents a parallel billion-dollar infrastructure that most mainstream market reports quietly undercount — or avoid entirely.

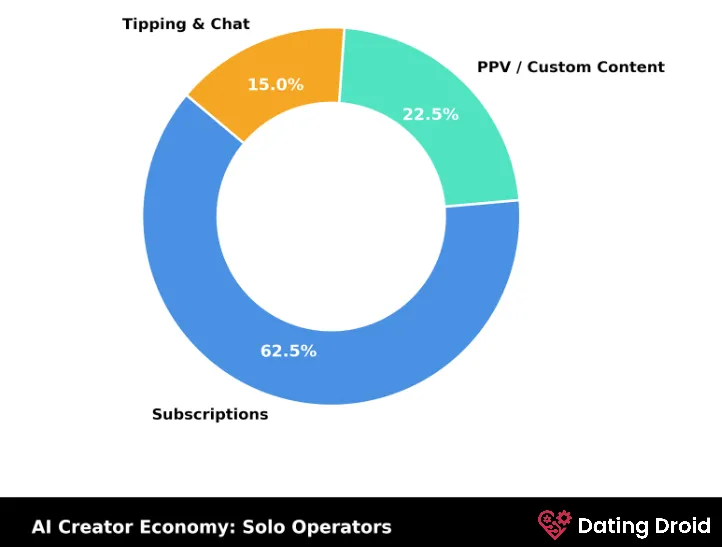

💰 AI Creator Economy — Solo Operators, Serious Earnings

Not all the money flows upward to platform companies. A serious and growing chunk is going to individual operators who have figured out how to use AI tools to build entirely virtual income streams.

How a typical active AI creator's monthly income breaks down:

| Revenue Stream | Share of Income |

|---|---|

| Subscriptions (Fanvue / OnlyFans) | 60–65% |

| PPV / Custom content requests | 20–25% |

| Tipping & chat sessions | 10–15% |

Custom and NSFW-specific content can account for up to 85% of total earnings for creators who go full explicit. The reason is not just content quality — fans are paying for the fantasy of personalised interaction, and they pay a premium for anything that feels made specifically for them.

Most serious AI creator operators work 10–15 hours per week after their initial automation workflows are built out. The leverage sits in the system architecture, not the daily content grind.

✅ Platform-Layer Revenue — The Silent Winners

Here is the part of the AI companion revenue story that rarely makes headlines: some of the biggest earners are not making content or building companion apps at all. They are running the infrastructure that everything flows through.

OnlyFans grossed $7.2 billion in 2024, with $1.4 billion in net profit — on a flat 20% platform cut. The platform has 4.19 million creators and requires that AI content must resemble the verified human creator, which limits purely synthetic personas but maintains its dominant position overall. The death of founder Leonid Radvinsky in early 2026 added some uncertainty, but the structural dominance of the platform as adult subscription infrastructure remains intact.

Fanvue hit $100M ARR in 2025, up from $40M in 2024 — a 150% year-over-year jump confirmed by Sacra. After Fansly banned photorealistic AI-generated content in June 2025, Fanvue became the only major adult subscription platform to fully embrace from-scratch synthetic creators. Their partnership with ElevenLabs ($330M ARR) enables AI creators to offer voice messages and phone calls — extending monetisation from images and text into audio. The platform now has 17 million monthly active users and 250,000 creators.

SexyFans runs an 80/20 creator-platform split, offering creators an alternative to the OnlyFans and Fanvue duopoly, with subscription tiers, PPV, and tipping mechanics across a hybrid dating-and-content format.

Feeld, operating in the niche relationship and kink-adjacent dating space, reported $66 million in sales and $12.5 million net profit in 2024 — a notably healthy margin for its size.

Platform businesses win structurally. They clip a percentage of every transaction regardless of which AI tool is trending, which creator is having their moment, or which NSFW niche is growing fastest this quarter.

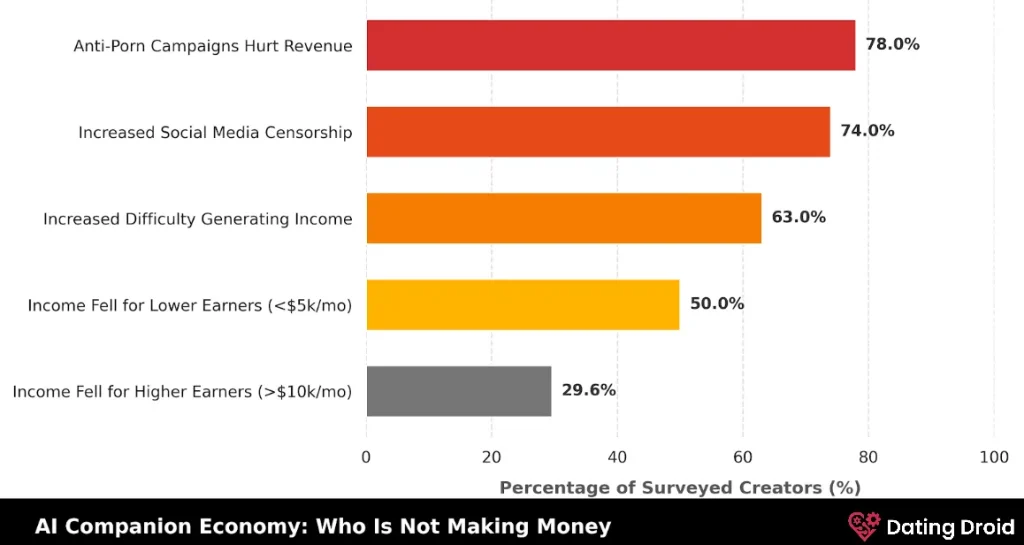

💸 Who Is Not Making Money (And Why)

Not everyone is eating, and a full picture of the AI companion revenue landscape requires being honest about the other side of the table.

On the app side, market concentration tells a similar story. The bottom 300+ apps are fighting over roughly 11% of total category revenue. Most generic companion apps follow a predictable arc: launch, get moderate downloads, fail to retain users emotionally, and exit quietly within 12 months.

The Appfigures data tracking this category explicitly excludes failed apps — meaning the actual number of attempts in the companion AI space far exceeds the 337 currently generating any revenue at all.

🌐 Revenue Geography — Where the Money Comes From

Geography shapes the revenue split in ways that do not always appear in the top-line market figures.

As Western markets tighten legislation around AI-generated adult content, the gap between regulated and unregulated markets in terms of per-user revenue will continue widening. Platforms that built web-first architectures early are already capturing that advantage.

(For a full breakdown of which platforms dominate downloads by region and operating system, see our AI Dating App Download Statistics piece.)

👀 Where the Revenue Flows Next

The $120M mobile app figure is a starting point, not a ceiling. The category is accelerating on nearly every metric.

Platforms that combine genuine emotional engagement with NSFW capability and creator monetisation tools have the clearest path to outsized revenue. The infrastructure for the next generation of virtual relationships is being built right now — and the companies building it are already printing money.

🎯 Your Burning Questions, Answered

Which AI companion app makes the most money?

Chai AI leads on pure app revenue at an $85M annualised run rate (April 2026). Fanvue tops the broader category at $100M ARR — but it runs creator infrastructure, not a companion app directly.

How do AI girlfriend apps make money?

Subscriptions are the backbone, stacked with freemium upsells, token packs, PPV drops, and tipping. The profitable ones never rely on just one stream.

What is revenue per download for AI companion apps?

$1.18 in H1 2025 — up 127% from $0.52 in 2024. Users went from browsing to actually paying, fast.

How much do AI companion creators earn?

Top Fanvue AI persona operators clear $20,000–$50,000/month. The median creator earns under $1,000/month. The gap is brutal and very real.

Why do the top 10% of apps earn 89% of revenue?

Emotional stickiness. Apps with memory, voice, and deep personalisation retain users who spend more and churn less. Generic chatbots cannot compete with that.

Is NSFW AI more profitable than mainstream AI companions?

Per user, yes — by a wide margin. The NSFW AI chatbot segment hit $400M annually in early 2026, while the broader mobile companion category sat at $120M. Adult intent converts faster and spends harder.

What is ARPU for AI girlfriend apps?

Blended ARPU on freemium platforms sits at $2–$5/month. On dedicated NSFW apps with PPV and tipping, paying-user ARPU runs $30–$80/month or higher.

📌 Conclusion

The AI companion industry revenue game has one rule: build emotional stickiness or go home broke.

Chai AI, Fanvue, Candy AI — three very different businesses, three very different strategies, one shared result: serious, compounding revenue. Meanwhile, 300+ apps are collectively fighting over 11% of the market.

The NSFW segment, the creator economy, and voice monetisation are all still in early innings. The platforms that crack the engagement loop — and keep cracking it — will own what comes next.

The money is already here. It is just not evenly distributed.

Stay Updated with Us